Everything You Need to Know About CSRD Reporting: Update & What to Watch for in 2026

What’s Changed Since 2023

Since the original Corporate Sustainability Reporting Directive (CSRD) rules were solidified in mid-2023, several updates and policy shifts have emerged that affect how companies should plan, collect, assure, and report sustainability data:

- Omnibus package & “Stop-the-Clock” relief

-

- The EU introduced an omnibus legislative package in February 2025, intended to simplify and streamline sustainability reporting, including CSRD, EU Taxonomy, Corporate Sustainability Due Diligence Directive (CSDDD), and the Carbon Border Adjustment Mechanism (CBAM) Regulations.

- A “Stop-the-Clock” directive delays certain reporting requirements for Waves 2 and 3 companies.

- Revisions to ESRS (European Sustainability Reporting Standards)

-

- On July 31, 2025, European Financial Reporting Advisory Group (EFRAG) released revised exposure drafts of the European Sustainability Reporting Standards (ESRS) aimed at simplification: reducing the number of disclosures, clarifying language, improving structure, reducing overlaps, and refining the double materiality assessment process.

- The consultation period for these drafts runs through September 2025, with final technical advice expected by end of November 2025.

- EU Taxonomy updates

-

- On July 4, 2025, a delegated act was adopted amending Taxonomy disclosures, simplifying reporting forms, adjusting the Do No Significant Harm (DNHS) criteria, and introducing materiality principles.

- These changes are expected to apply from the 2025 financial year (i.e. reports published in 2026), though there is some flexibility: companies may be able to postpone applying certain new rules by one year.

- Phase-in of reporting timelines & shifting thresholds

-

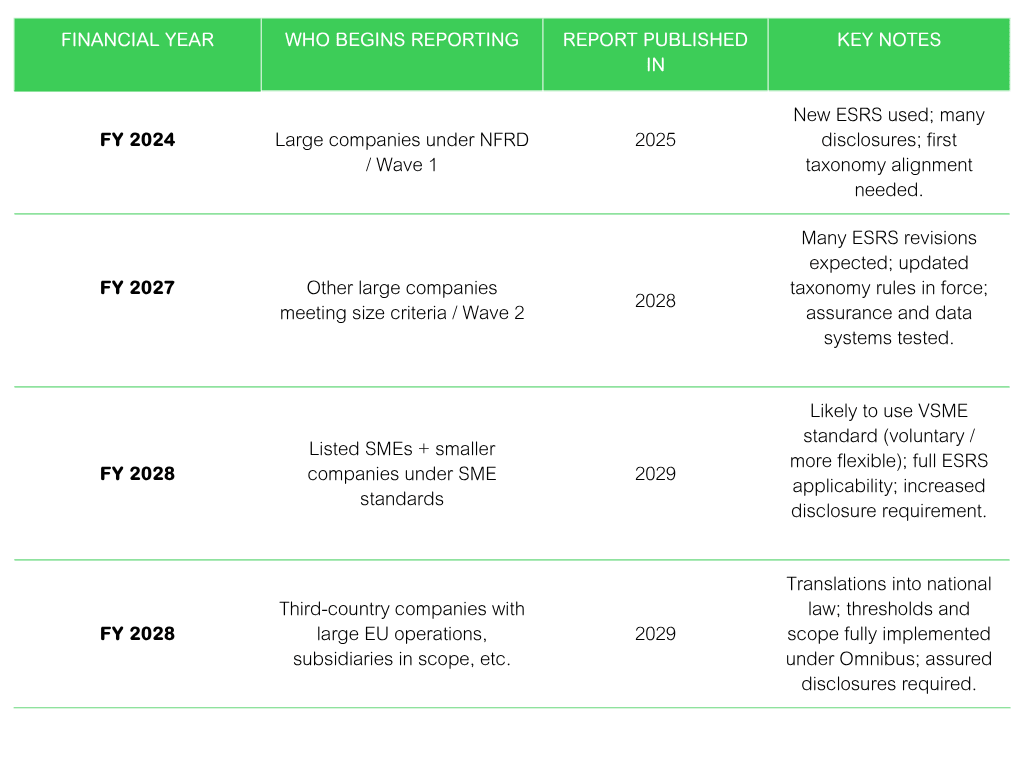

- Many large, EU-based companies (especially those already under the Non-Financial Reporting Directive, NFRD) began CSRD/ESRS-compliant reporting for FY 2024 (published in 2025).

- Starting FY 2028, other large companies meeting size/turnover/assets criteria will report (for data in 2027, published in 2028).

- For listed Small & Medium Enterprises (SMEs), standard reporting under ESRS is expected to begin for FY 2028 (= reports in 2029).

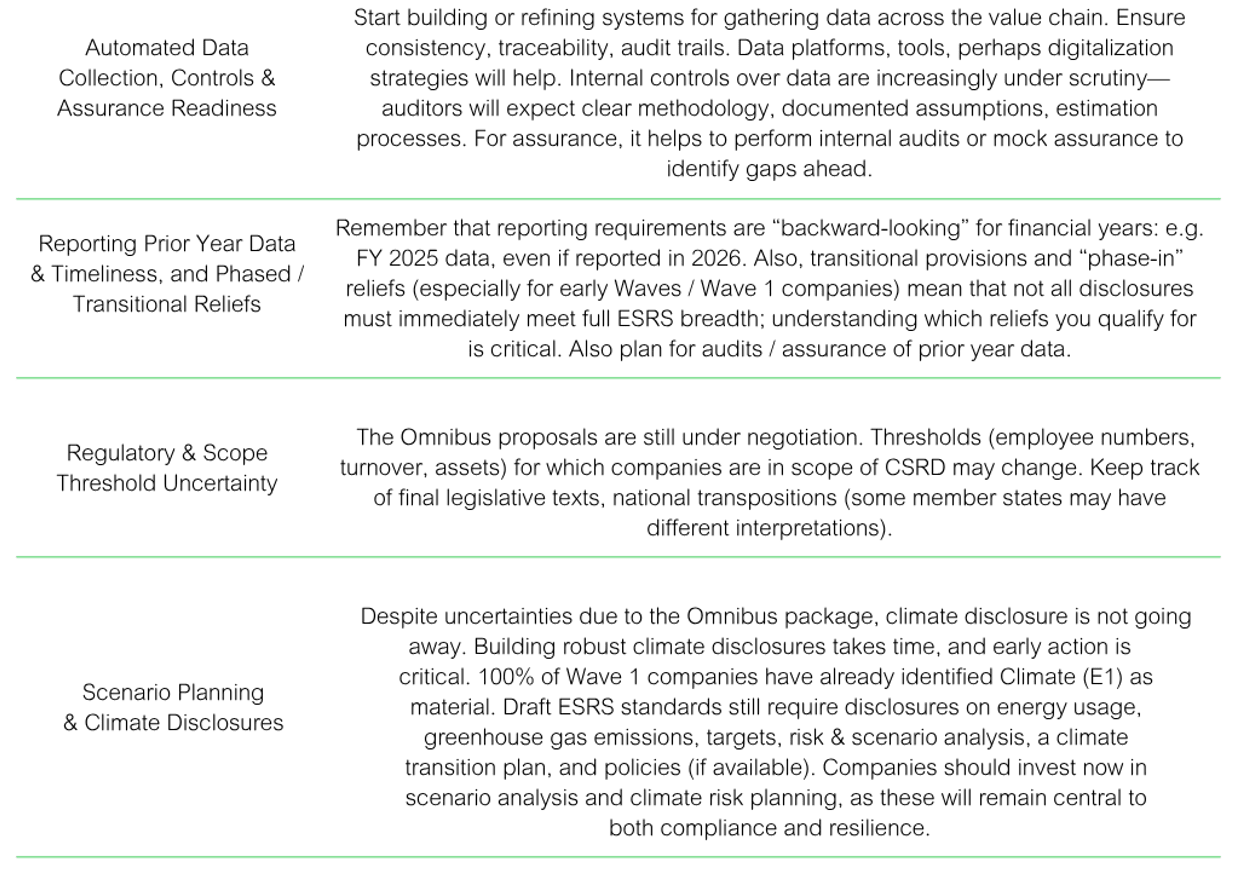

- Assurance requirements & data readiness

-

- CSRD requires third-party limited assurance over reported sustainability data.

- Because of the increasing scope and detail (especially for Scope 3 emissions, environmental/social topic disclosures, etc.), automated data collection, robust controls, data governance and audit readiness are essential. Treat manual and ad-hoc systems as high risk.

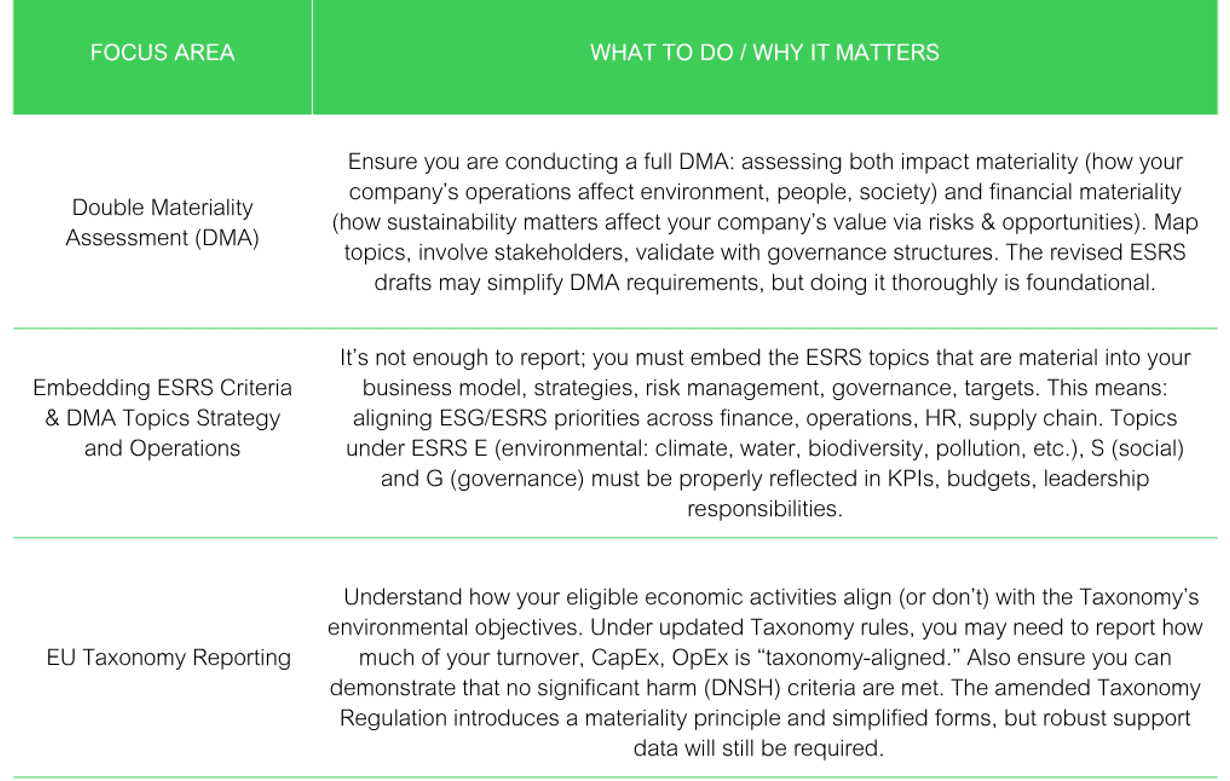

Key Considerations Heading Into 2026

As companies gear up for more comprehensive reporting requirements, here are the areas that demand attention:

EU Taxonomy as Part of CSRD Reporting: Key Details & Timeline

- The EU Taxonomy Regulation is tightly integrated into ESRS / CSRD disclosures. Under Article 8 of the Taxonomy Regulation, non-financial and financial undertakings are required to disclose alignment of their business activities (turnover, CapEx, OpEx) with sustainable economic activities as defined in the Taxonomy.

- The Delegated Act of July 4, 2025 introduced changes including simplified reporting formats, clearer “Do No Significant Harm” (DNSH) criteria, and a materiality principle for taxonomy disclosures.

- Implementation date for many taxonomy changes is for financial year 2025 (i.e. reports published in 2026), though transitional options (delays) exist for some companies.

What You Must Do Now If You Are Under CSRD or Will Be Soon

To ensure compliance and strategic advantage, start taking action now:

- Perform or refine your double materiality assessment

-

- Engage stakeholders, map impacts / dependencies, quantify both environmental/social impacts and financial risks/opportunities.

- Use this to identify material ESRS topics for your business.

-

- Set up data infrastructure & internal controls

-

- Identify data owners (finance, operations, procurement, supply chain, etc.).

- Invest in systems (automated or semi-automated) to collect data (especially for Scope 3 emissions, other environmental/social metrics).

- Ensure audit trails, estimation methods, and assumptions are documented.

-

- Plan for assurance

-

- Early engagement with assurance providers.

- Run internal mock assurance to test readiness.

- Understand what “limited assurance” assurance” entails under ESRS / CSRD.

-

- Align sustainability strategy / governance to ESRS topics

-

- Incorporate material topics into strategic plans, KPIs, budgets, reporting lines.

- Ensure governance oversight (board / senior leadership) is clear.

-

- Monitor legislative developments & threshold changes

-

- Keep track of final Omnibus outcomes and national transpositions.

- Pay attention to when you will come into scope under revised thresholds / waves.

-

- Report on prior year’s data in required formats

-

- If you are already in scope, ensure you have data for FY 2024, FY 2025, etc., as required.

- Use digital, machine-readable formats (ESEF / electronic formats / taxonomy tagging) where needed.

-

Looking Ahead to 2026 and Beyond

- Expect simplified ESRS standards to become law following the consultation and adoption phases in late 2025 / early 2026. These will reduce disclosure burdens, clarify language, streamline double materiality requirements.

- Taxonomy reporting will become more mature, with greater precision in alignment / alignment metrics, improved DNSH implementation, perhaps additional economic activities being added.

- Assurance expectations will likely tighten—“limited assurance” may give way to higher assurance for certain disclosures.

- Non-EU companies with exposure or supply chain ties to the EU should anticipate requests for ESG / taxonomy data even if not directly in scope.

- The importance of transparency, comparability, and interoperability (with ISSB, GRI, etc.) will increase as stakeholders (investors, regulators, customers) demand reliable data.

Conclusion

CSRD reporting is no longer just a box-ticking exercise; it is a strategic imperative. Since 2023 we have seen meaningful shifts: simplification in progress, revised standards under development, taxonomy adjustments, and growing expectations for data quality, assurance, and embedding sustainability deeper into business practices.

Companies preparing for CSRD / ESRS reporting in coming years (especially those with FY 2025 data to report in 2026) should invest now in:

- double materiality assessments,

- strong data and control systems,

- reporting strategy aligned with ESRS criteria,

- and readiness for assurance.

Staying ahead won’t just ensure compliance — it can unlock trust, resilience, and competitive advantage.

Schneider’s global subject matter experts are well-versed in the CSRD rules and the impacts of this important reporting directive in-region. We encourage you to connect with our team to help navigate this regulatory future. Click here to get started.

Sign up for our upcoming webinar, "The Clock’s Stopped but the Pressure’s On in 2026: CSRD Readiness in North America" on November 20, 2025.

Timeline at a Glance

Contributor:

Kristi Plume, Senior Manager ESG Consultancy