Navigating the One Big Beautiful Bill Act: Strategic Implications for Sustainability-Focused Businesses

The enactment of the One Big Beautiful Bill Act (OBBBA)(H.R.1) represents a pivotal moment in the evolution of U.S. clean energy policy. For private sector organizations committed to decarbonization, energy efficiency, and sustainable supply chain transformation, the legislation introduces a new set of constraints—and opportunities—that demand strategic recalibration.

The enactment of the One Big Beautiful Bill Act (OBBBA)(H.R.1) represents a pivotal moment in the evolution of U.S. clean energy policy. For private sector organizations committed to decarbonization, energy efficiency, and sustainable supply chain transformation, the legislation introduces a new set of constraints—and opportunities—that demand strategic recalibration.

Below, we outline the most consequential provisions of the Act that relate to corporate energy and decarbonization, and what they mean for businesses that have been leveraging the Investment Tax Credit (ITC), Production Tax Credit (PTC), and other Inflation Reduction Act (IRA) incentives.

.

1. Accelerated Phase-Out of Clean Energy Tax Credits

The OBBBA significantly compresses the timeline for accessing key clean energy tax incentives:

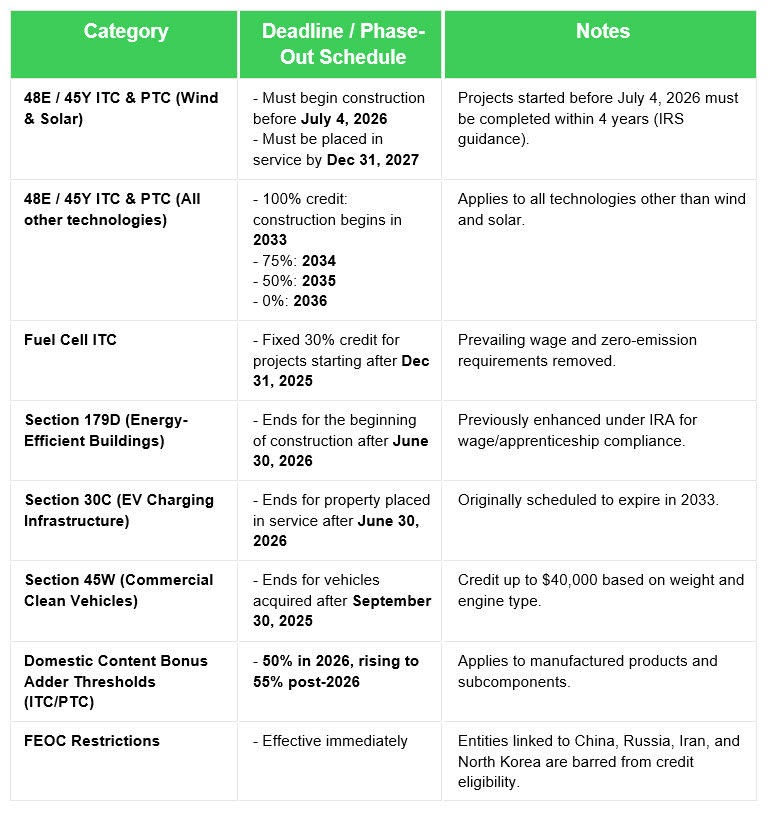

- Wind and Solar Investment (48E) and Production (45Y) Tax Credits:

- Beginning of construction before July 4, 2026, must be placed in service within 4 years to qualify for the tax credits.

- Projects initiated after that date must be placed in service by December 31, 2027, to qualify.

- For all other eligible technologies (nuclear, hydro, geothermal, battery storage, etc.), the 48E ITC and 45Y PTC credits phase out as follows:

- 100% of the credit value for construction beginning in 2033 or earlier

- 75% of the full credit value in 2034

- 50% of the full credit value in 2035

- Fully sunset by 2036

Strategic Insight: Developers with clean energy projects in the pipeline must act swiftly to begin construction. Many will need to secure a power offtake agreement, like a corporate PPA, in the next 6-10 months in order to start construction and qualify for the tax credits. Delays in development or permitting could result in the forfeiture of critical tax benefits that were previously expected to remain available through the next decade.

Strategic Insight: Without the tax credits, renewable energy prices are set to rise between 10 and 50%. There is still significant electricity load growth forecasted in the US due to AI/data center demand among other factors. This combination of higher-priced supply and increasing demand is likely to drive up electricity prices significantly in most markets across the US in the mid to long term.

Strategic Insight: Tax credits remain transferrable. Companies that have been considering or taking advantage of tax credit transfers will have a runway to continue to pursue this method of supporting the energy transition and reducing tax burden.

.

2. New Restrictions on Foreign Entities of Concern (FEOC)

To reinforce national security and domestic supply chain resilience, the Act imposes strict limitations on the use of components sourced from certain foreign entities:

- Entities affiliated with or materially supported by China, Russia, Iran, or North Korea are barred from participating in projects eligible for clean energy tax credits.

- The Treasury Department is expected to issue safe harbor sourcing tables by the end of 2026 to guide compliance.

- ITC Projects must meet escalating thresholds to qualify for the domestic content adder:

- 45% for beginning of construction in 2025, 50% in 2026, rising to 55% for beginning of construction after 2029 (ITC/PTC)

- This change serves to align the ITC domestic content adder criteria to the PTC's already-in-place criteria

Strategic Insight: Renewable energy developers must proactively assess and restructure their supply chains to ensure compliance. This includes evaluating supplier ownership structures, sourcing origins, and material traceability, particularly for solar, battery, and EV-related components. For corporate power offtakers, it will be critical to perform strong due diligence on any project to ensure it will qualify for the tax credits.

.

3. Early Sunset and Realignment of Key Incentives

In addition to phasing out core tax credits, the OBBBA accelerates the termination of several other sustainability-related incentives and modifies eligibility for emerging technologies:

- Section 179D: The energy-efficient commercial building deduction ends for projects starting after June 30, 2026.

- Section 30C: The EV charging station credit ends for property placed in service after June 30, 2026.

- Section 45W: The commercial clean vehicle credit ends for vehicles acquired after September 30, 2025.

- Fuel Cell ITC: A fixed 30% credit remains available for beginning of construction after December 31, 2025, but without prevailing wage or zero-emission requirements.

- Section 45Q Carbon Capture Credit: Enhanced values remain—$85/ton for industrial capture and $180/ton for direct air capture—but are subject to FEOC restrictions.

Strategic Insight: While some technologies remain eligible for support, businesses must carefully evaluate project structures, sourcing, and timelines to ensure continued eligibility. Companies planning to electrify fleets, install EV infrastructure, or pursue energy-efficient retrofits should accelerate development to preserve access to these incentives.

Executive Perspective: Why Timing Is Everything

— John Powers, Global VP, Renewable Energy Advisory, Schneider Electric

.

As John Powers explains in his recent message, the OBBBA has created a narrow but critical window for organizations to act. With tax credits phasing out faster than expected and electricity demand on the rise, the next year presents a unique opportunity for corporate buyers to secure renewable energy at favorable terms.

Ready to meet your decarbonization goals before incentives fade and markets tighten?

Join our live webinar to explore how the OBBBA could impact your strategy—from supply chain to reporting—and learn how to move forward with clarity and speed. Reserve your spot today.

What This Means for Sustainability-Focused Businesses

Accelerate Strategic Planning

Organizations must reassess project pipelines and timelines to ensure alignment with the new eligibility windows. Early-stage projects should be prioritized for development and financing.

Strengthen Supply Chain Governance

Compliance with FEOC restrictions will require enhanced due diligence, supplier engagement, and potentially reshoring or diversifying sourcing strategies.

Reevaluate Capital Allocation

With the early sunset of several incentives, businesses should revisit the financial assumptions underpinning planned investments in EV infrastructure, clean fleets, and energy-efficient buildings.

Explore Emerging Opportunities

While some credits are being phased out, others—such as battery storage—remain robust. Companies may benefit from pivoting toward technologies and strategies that continue to receive federal support.

Summary of the newly phased deadlines and eligibility thresholds introduced by the One Big Beautiful Bill Act (OBBBA) across key clean energy categories:

If your organization is navigating the implications of the OBBBA and needs guidance on how to adapt your sustainability strategy, our team is here to help. We offer tailored advisory services to help you stay compliant, competitive, and climate-forward.

Please reach out to our team to connect with a Schneider Electric Sustainability Business renewable energy expert.