The APAC Executive's Guide to ISSB and CSRD Reporting

Charting the Course in Sustainability Reporting: The APAC Executive's Guide to ISSB and CSRD

,

The International Sustainability Standards Board (ISSB) and Corporate Sustainability Reporting Directive (CSRD) have emerged at the forefront of the reporting landscape. They present critical implications for corporates internationally and in the Asia Pacific (APAC) region: for instance, key geographies such as Singapore, Malaysia, and Hong Kong begin their first ISSB reporting year in 2025. This article addresses the reporting requirements for APAC companies regarding either or both standards and provides insights on how companies can approach the sustainability reporting journey efficiently.

The International Sustainability Standards Board (ISSB) and Corporate Sustainability Reporting Directive (CSRD) have emerged at the forefront of the reporting landscape. They present critical implications for corporates internationally and in the Asia Pacific (APAC) region: for instance, key geographies such as Singapore, Malaysia, and Hong Kong begin their first ISSB reporting year in 2025. This article addresses the reporting requirements for APAC companies regarding either or both standards and provides insights on how companies can approach the sustainability reporting journey efficiently..

ISSB and CSRD: Two frameworks to guide sustainability reporting

The ISSB and CSRD are poised to transform the sustainability reporting space, with the former announced in 2021 at the 26th Conference of Parties (COP26) in Glasgow, and the latter approved in 2023 for implementation in the European Union (EU).

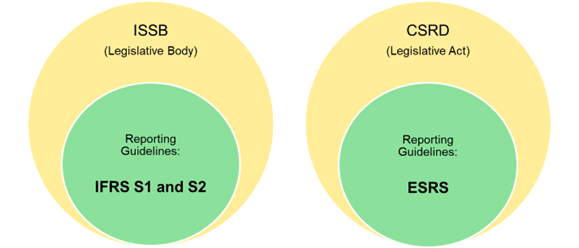

Created by the International Financial Reporting Standards (IFRS) Foundation, the ISSB is an internationally recognized organization that aims to consolidate existing voluntary sustainability reporting initiatives and enable corporate disclosures that are actionable and comparable. In June 2023, the ISSB released the IFRS S1 and S2 reporting guidelines (see Figure 1), establishing a high-quality global baseline of investor-focused sustainability disclosures.

The CSRD is a legislative act enacted by the EU to create a mandate and to enhance corporate transparency surrounding sustainability practices. The EU released the European Sustainability Reporting Standards (ESRS) in July 2023 (see Figure 1), which contains 12 standards (2 cross-cutting and 10 topical) and aims to enhance consistency and accuracy of sustainability disclosures of companies operating in the EU. It is in the process of integration into the local legislation of countries in the EU, with varying degrees of readiness across the region.

.

Figure 1: A simple overview of the ISSB and CSRD, visual generated by Jesslyn Dharma

.

Each standard requires a wide range and amount of data for disclosure, and this multiplies should companies need to fulfill both. Some APAC companies may need to comply with either or both standards, making it essential for them to understand overlapping requirements to streamline their reporting activities. For instance, companies with listed securities, operations, or subsidiaries in the EU market, will need to prepare for CSRD and may soon be subject to ISSB standards. The next section will elucidate these applicability requirements in further detail and the expected timeline for their adoption.

.

Applicability of ISSB and CSRD in Asia Pacific

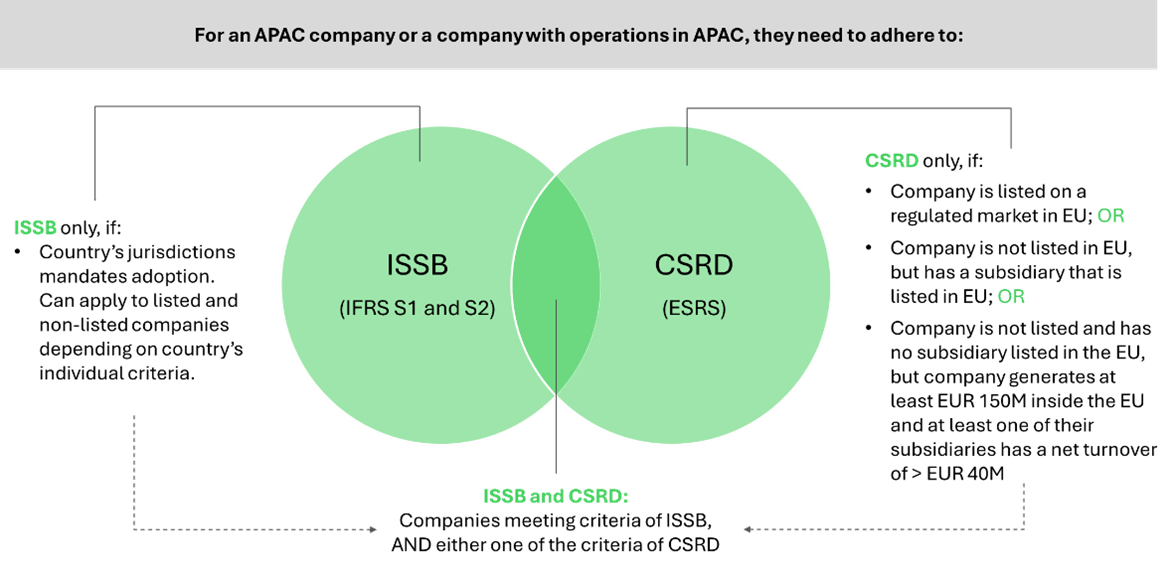

Companies should first identify whether they need to comply to ISSB and/or CSRD, using Figure 2 as a guide.

.

Figure 2: Breakdown of individual qualification criteria for ISSB and CSRD compliance as a guide for companies, visual generated by Jesslyn Dharma

.

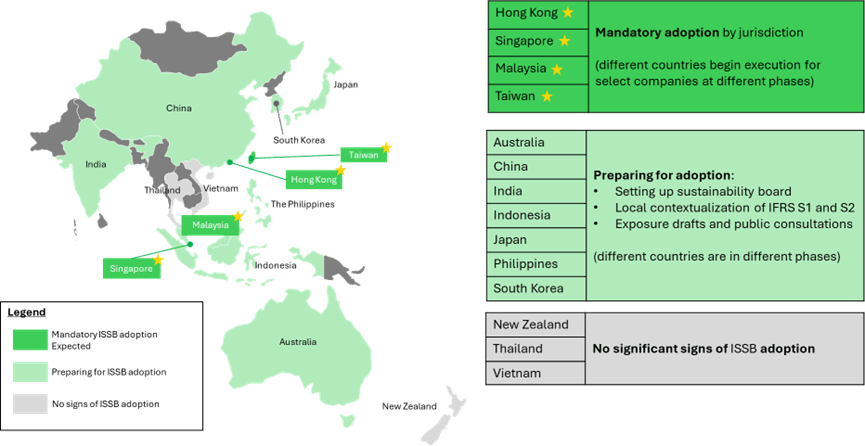

Diving deeper into individual standards, ISSB compliance is only mandatory for companies in jurisdictions that have adopted the standard. This is true globally and not limited to APAC. Figure 3 illustrates the different stages of ISSB adoption across APAC and when it will come into effect for countries that have confirmed its adoption.

.

Figure 3: Adoption Landscape of ISSB and CSRD in the APAC region (October 2024), visual generated by Jesslyn Dharma

.

From the observations of countries that have confirmed the adoption of ISSB in APAC – which consists of Singapore, Hong Kong, Malaysia, and Taiwan , the rollout of mandatory ISSB reporting will begin with companies listed in the respective regulated markets. Each of the countries will have their unique execution plan. For instance, Malaysia’s rollout of mandatory ISSB reporting will be carried out in phases, starting with large-listed companies in the main market with market capitalization of RM2 billion and above to publish a report by 2025. This will be followed by other listed companies in the main market by 2026, and listed companies in the Alternative Capital Exchange (ACE) market, as well as non-listed companies with annual revenue of RM2 billion or above by 2027. As Figure 3 shows, other countries within APAC are gearing up to adopt ISSB, and adoption is expected to grow in the future.

.

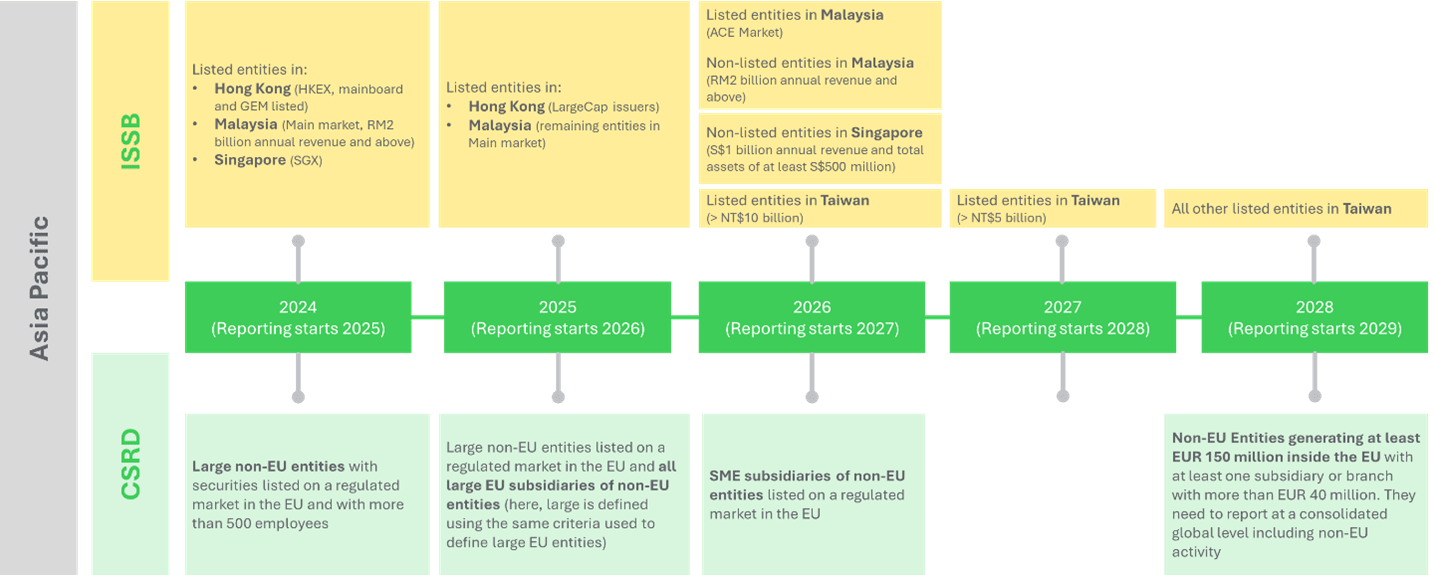

As for CSRD, mandatory compliance is not determined by the individual APAC jurisdictions, instead, it depends on whether companies fall under the scope outlined by the legislative act. APAC, companies that need to be aware of CSRD compliance are those mentioned in Figure 2. The compliance timeline varies based on the category of each APAC-based company. Figure 4 below illustrates the effective reporting year for CSRD compliance for APAC companies, and outlines the corresponding ISSB requirements for those APAC countries which have confirmed its adoption.

.

Figure 4: CSRD and ISSB timelines of adoption for APAC countries (October 2024), Visual generated by Jesslyn Dharma

.

Source: IFRS Foundation, European Commission

.

Referring to the diagrams above, APAC companies can determine whether they need to comply with either ISSB, CSRD, or both, along with the effective dates for each reporting requirement. With this information, companies can begin their sustainability reporting journey. However, the complexity and overlapping requirements in the reporting landscape may lead to confusion and challenges. The next section outlines significant challenges that companies might face.

.

Challenges companies face with sustainability reporting

Companies in the APAC region encounter two significant challenges when embarking on the sustainability reporting: compliance complexity and knowledge gaps in fulfilling reporting requirements, as well as data management.

.

The first challenge is ensuring full compliance across multiple reporting standards. This is particularly pressing for APAC companies that discover they are subject to both the ISSB and CSRD regulations. This challenge is unique to APAC and other non-EU companies with a qualifying presence in Europe.

.

This matter is further complicated by two key factors. First, the assessment criteria vary by the framework: while ISSB focuses solely on how climate change impacts businesses, CSRD requires double materiality, which mandates companies to disclose their environmental impact in addition to how their business is impacted by climate change. Second, these standards will be implemented in a short period of time, with ISSB likely to be enacted first for APAC companies, followed by CSRD, which could lead to inefficient resource allocation and reporting process should companies be unaware of the overlapping and distinct requirements of these two standards from the outset, potentially leading to duplicative efforts. As a result, harmonizing the requirements of these different standards into a cohesive sustainability report is a significant challenge for APAC companies. They must consider both their host country's reporting obligations, ISSB, and those of the EU through CSRD compliance.

.

The second major challenge companies face is managing the often-overwhelming amount of data from their operations to meet the requirements of their sustainability disclosures. According to the 2024 ESG Practitioner Survey, 79% of companies in Singapore revealed that collecting accurate data to fulfill stringent CSRD requirements will be a challenge for their organization. Assessing as many as hundreds of data points from a double materiality perspective to meet the rigorous disclosure standards for the reporting frameworks is an onerous task to complete, especially if the company’s scope of operations covers a wide area.

.

Schneider Electric’s Sustainability Business, in collaboration with our EcoAct team, is uniquely positioned to support companies with these major challenges relating to ISSB and CSRD through our portfolio of services, bringing international standard compliance advisory experience, bespoke gap assessment exercises, stakeholder engagement programs and data-driven solutions such as EcoStruxureTM Resource Advisor to establish data protocol and governance for on-going compliance. We provide broad climate advisory solutions such as double materiality, gap analysis, IT system reconfiguration support, assurance support, and climate risk management. We help clients achieve compliance and look beyond for broader sustainability-driven transformation opportunities.

.

Conclusion

From 2025 onwards, the ISSB joins CSRD as the newest sustainability reporting framework to be mandatory in select types of companies and geographies within APAC. Sustainability reporting is a big undertaking, both necessary for business compliance and a powerful tool for business success. How will your company navigate this increasingly complex reporting landscape? Schneider Electric, voted the most Sustainable Company in the World 2024 by Times Magazine and Statista, has local presence in the APAC region to serve you. Our Sustainability Business teams support 40% of the current Fortune 500 companies with climate advisory. Learn more about ISSB from our existing Schneider Perspectives articles here and here, as well as cross-border reporting for CSRD articles here and here.

.

For further guidance on sustainability reporting within the ISSB and CSRD, please contact us , and subscribe to receive the latest Asia-Pacific energy and sustainability perspectives.

.

About the Authors:

This was researched and written by members of the Sustainability Business Knowledge Hub Team in the Singapore Office: Clara Seet, a Sustainability Analyst; Jesslyn Dharma, a Schneider Graduate Program Associate; Sean Neo, a Schneider Graduate Program Associate; and Tanya Paul, a Sustainability Consultant.

They wish to thank Alister Stewart, Bernard Kwok, Hemy Bae, Olivia Gao, Seooh Chae, and Sofia Tyebally for their contributions to this perspective.