Are Data Centers and Colocation Providers Prepared for the Evolving Energy Market?

Market evolution is driving change in how companies strategically manage their energy. This changing landscape opens opportunities for businesses to modify their energy consumption mix, with potential cost savings as a result. Increases in data-driven technology also help companies better understand their real-time, interval energy consumption and demand, which can provide the visibility required to curtail usage when prices spike or better negotiate contracts according to individual site consumption and demand patterns.

Strategic energy management can result in significant cost savings. But respondents to our recent corporate energy and sustainability research report indicate strategic sourcing as a top savings opportunity only 29% of the time. This is unfortunate, as businesses with strategic sourcing initiatives are also more likely to explore innovative technologies and invest in other complementary technologies such as combined heat and power, battery storage and renewables.

There’s also increasing complexity in energy sourcing as markets begin to diversify their generation mix. Renewable technologies are now some of the most affordable electricity sources in the world and the result is higher renewable penetration than ever before.

The upside to this market evolution is that cloud-service, colocation, and data center companies have an immense opportunity to save money and balance their generation sources. But this opportunity also comes with a downside: the need to manage energy and risk in a more nuanced and strategic way.

Change is Afoot: How the Market is Evolving

Market evolution introduces new considerations for technology companies to weigh as part of their overall procurement strategy. No longer is renewable energy an add-on for only the most progressive and environmentally-minded organizations. Renewables have become a key business strategy for many companies in the cloud-service and data center space, an industry that consistently leads the way in annual procurement of renewables via long-term corporate power purchase agreements (PPAs).

Data center and cloud-service providers are consistently ranked among the largest users of renewable energy. In 2019, Equinix, Digital Realty, Salesforce and Iron Mountain are listed in the U.S.

Some evidence of the changes being driven by market evolution:

- Renewables are becoming central to business. Corporate investment in renewable energy continues at a rapid pace; 2018 was a record-breaking year with 13.4 GW of renewable energy contracts executed by corporations, and 2019 is predicted to follow this path. More than 150 corporations globally have committed to 100% renewable energy, with cloud-service and data companies being among some of the founding members of the RE100 initiative.

- Energy buyers are becoming more sophisticated. At the most basic level, energy buyers that used to simply accept the traditional grid electricity mix and pricing are getting more strategic about how, when and what type of energy they use. Organizations that buy energy attribute certificates (EACs) are now exploring contractual instruments in some of the most challenging global markets to advance development and meet procurement or carbon-reduction goals. Companies executing long-term PPAs are testing new collaborative solutions, such as aggregated buying, and innovative contract terms and structures like cap and collar or Microsoft’s VFA. Exploration and adoption of microgrids is on the rise. And some companies are exploring all these options—and more.

- To meet diverse goals, companies need cross-silo collaboration. It’s becoming imperative for companies to align on energy activities across traditional procurement, renewables, efficiency and sustainability, with data as the major intersection. Some companies go beyond simply aligning activities and sharing data; the most forward-thinking organizations expect to fully integrate sourcing and reporting for traditional energy and renewable energy into an active energy management strategy.

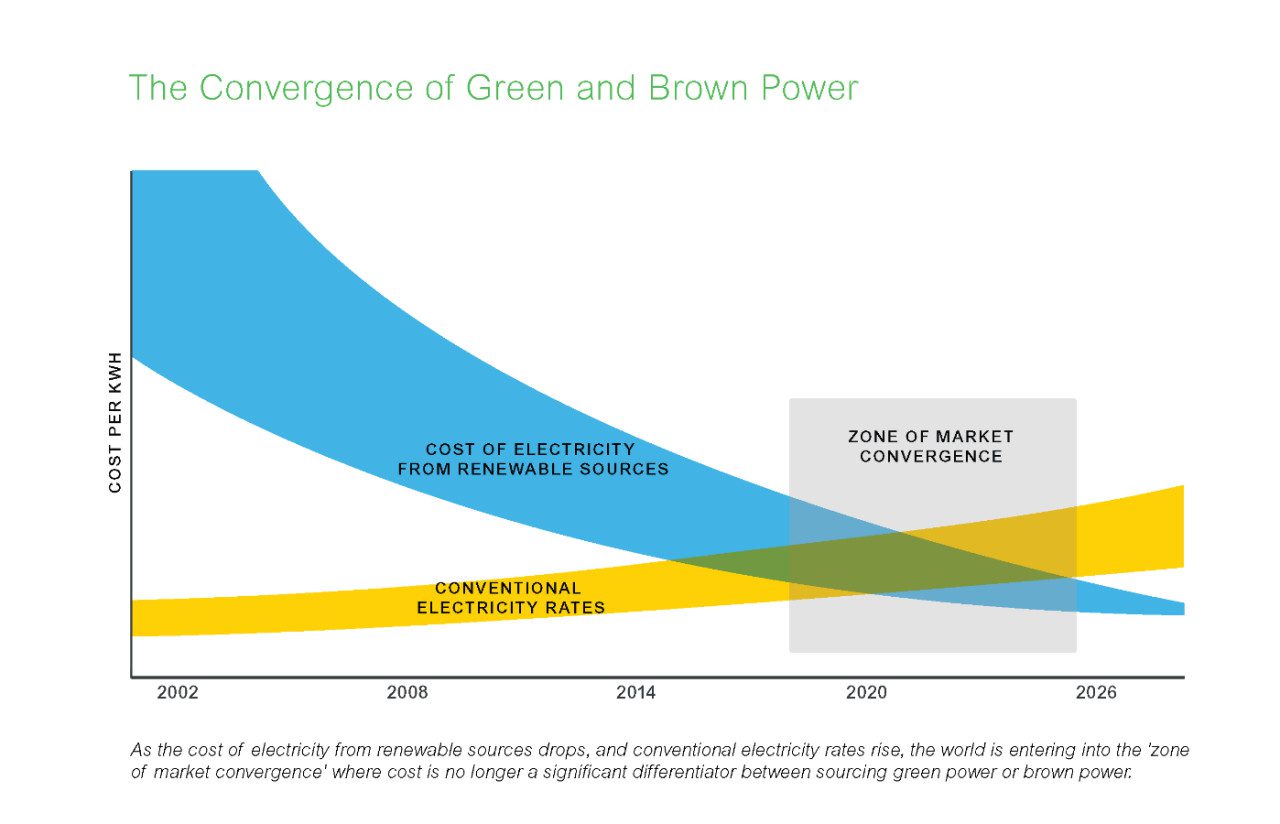

The Convergence of Green & Brown Power Drives Evolution

Emerging price parity of green power (such as wind and solar) and brown power (power traditionally supplied by the grid) is a cornerstone of the evolution of the energy market. The cost of wind and solar power have been on a swift decline for the past decade, bolstered by subsidization and increasing efficiencies in both technology and scale. As a result, renewable penetration on the grid has now reached roughly 33% globally, with increasing adoption forecast. This growth means that, alongside traditional brown power options for electricity, green power is now emerging as a more cost-effective choice. It also means that there are more suppliers in the market than ever before, and organizations in deregulated retail regions can now potentially evaluate green and brown power procurement on a level playing field.

Source: Schneider Electric – based on indicative, not actual, market prices.

How is convergence likely to impact your business?

- Green power will become more accessible. If you haven’t already, you will begin to see increasing access to green power options around the world. The low price—and increasing demand for fossil-free generation—means that there has never been a greater opportunity to adopt renewables.

- Adopting green power will be more cost-effective. Green power options are increasingly affordable, and for those solutions that may require a CapEx investment (such as an owned, onsite solar system), energy efficiency and energy-as-a-service solutions are potential avenues towards financial enablement.

- And companies will find synergies by breaking down organizational silos. The resulting combination of strategic sourcing, renewables procurement and efficiency form the basis for a more sophisticated integrated and cost-saving energy solution. Organizations are more likely to begin purchasing bundled services from electricity providers than can address their energy needs holistically as a result.

- But buyers must be aware when new opportunities emerge. As existing energy service providers take more innovative approaches to their services, and new providers enter the market hoping to capitalize on this growing need, organizations must be critical of any service offer, and ensure that it provides the greatest benefit with the lowest exposure. For instance, it can be attractive to companies to accept green power solutions provided by their traditional power supplier to streamline complexity. However, these solutions should be assessed alongside other available options in the market, to ensure you do not lock into a deal that exposes you as a buyer to unnecessary risk.

Navigate the Market Convergence

Fundamental changes in the generation mix are driving market evolution and making it more complex than ever for technology companies to purchase energy. An independent advisor like Schneider Electric Energy & Sustainability Services can help you evaluate your choices as the market converges to ensure you get the best products at the best price for your needs.

To learn more about how to navigate market convergence, the associated opportunities and challenges and how your company can prepare, watch our recent webinar with Smart Energy Decisions.